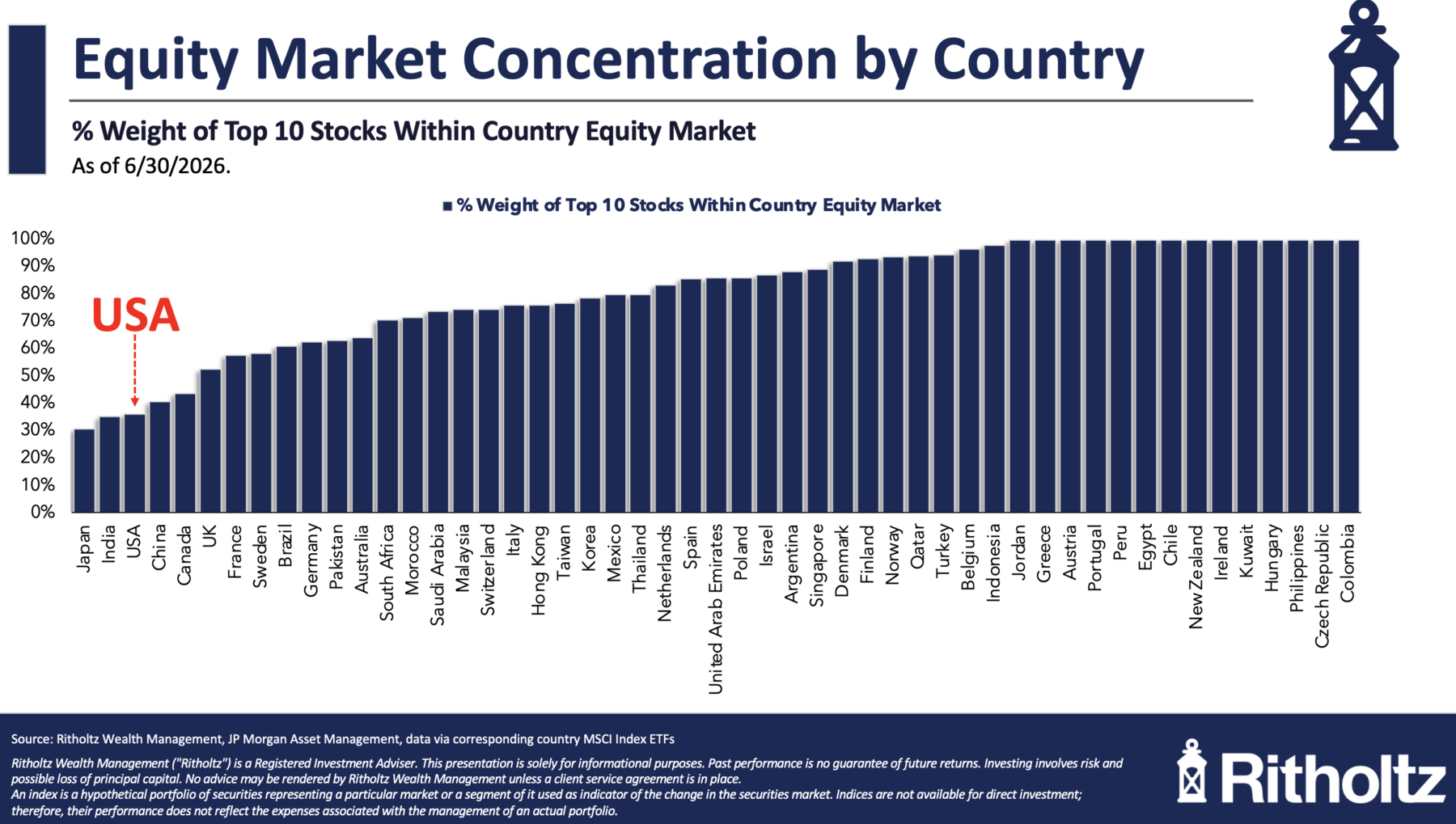

Research links: volatility estimates

Tuesdays are all about academic (and practitioner) literature at Abnormal Returns. You can check out last week’s edition including a look at...

AI

- How to use NotebookLM to review venture capital docs. (avc.xyz)

- On the dangers of letting AI read your fund documents. (ludovicphalippou.substack.com)

Asset management

- Unconscious bias is a factor in portfolio manager hiring. (klementoninvesting.substack.com)

- Good luck! How to get a quant job on the buy side. (byfire.substack.com)

Research

- Why you can't compare market P/E ratios over time. (manuinvests.substack.com)

- Why your intuition about long term fund performance may be wrong. (jeffreyptak.substack.com)

- Volatility measures are always an estimate. (concretumgroup.com)

- On the risks of single-stock ETFs. (alphaarchitect.com)

- A Q&A with Cullen Roche, author of "Your Perfect Portfolio: The Ultimate Guide to Using the World's Most Powerful Investing Strategies." (abnormalreturns.com)

- A round-up of recent white papers including 'Fresh Snow: Risk Management for Investment Systems.' (bpsandpieces.com)

Share

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0